Ensuring market liquidity before the market liberalization

July 2020

ANRE has issued an order amending the obligation of gas producers to sell on centralized markets and introduced a gas release program. Through this, between June 1, 2020 and December 31, 2022, the Romanian natural gas producers whose annual production, in the previous year, exceeded 3,000,000 MWh (Romgaz and OMV Petrom) have the obligation to sale on the centralized markets active in Romania (at this moment OPCOM and BRM) 30% of their production.

The order established the types of contracts and most important the amount of gas that should be offered monthly, as a percentage from the quantity of gas that will be offered to the market. Therefore, Romgaz and OMV Petrom are obliged to launch each month gas offers for monthly (30% of the quantity), quarterly (20% of the quantity), seasonal (warm season, cold season, 20% of the quantity) and yearly (30% of the quantity) standard products, as follows:

- Monthly products for each month starting with 2 months before start of deliveries;

- Quarterly products for each quarter starting with 4 months before start if deliveries;

- Season and annual products for each season/year starting with 7 months before the start of deliveries

These products will be offered on the double competitive platforms of both OCOM and BRM, where both BIDs and ASKs are anonymous and could not be differently highlighted from the other offers on the platforms, thus creating the possibility for other companies, producers or traders, to sell at similar levels. In this respect, ANRE’s order has been introduced to create competition and increase market liquidity.

Previous legislation still in force, created the obligation for gas producers to conclude each year standard contracts on centralized markets for at least 50% of the gas quantity delivered during that respective year. Contracts concluded under the gas release program will be counted within the 50%, not additionally.

One of the most important provision of the gas release order is the maximum starting price formula that will be used monthly from 1st of June 2020 until 31st of December 2020. This formula is linked 80% to the previously concluded contract on the Romanian market and 20% to the Central European Gas Hub (CEGH) index, applied for each contract. Therefore, for the quantities that will be offered in June 2020, as the order dose not take into consideration local trades concluded before 1st of June, the maximum price on the sell side will be 95% of CEGH Price.

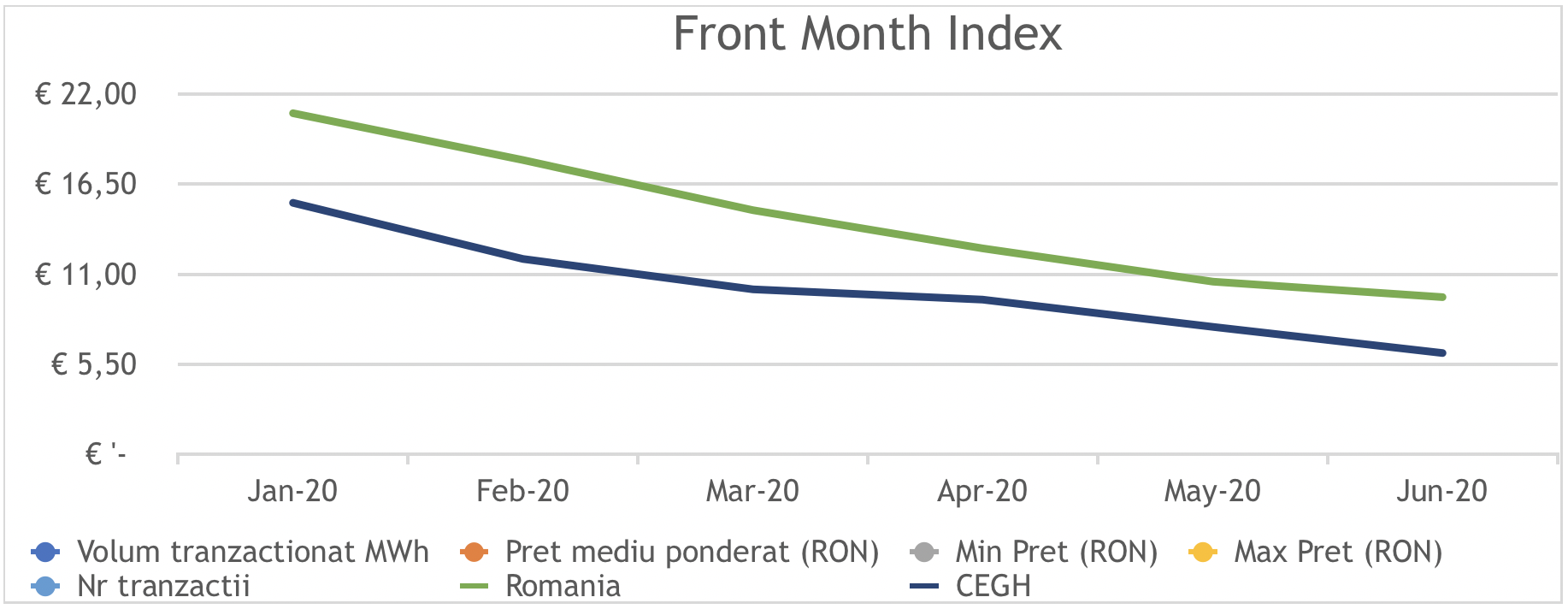

The potential impact of this regulation on the local wholesale market, especially on the short term, could be significant. As seen bellow, the Romanian gas market has been trading on a premium, compared to the CEGH or other western markets, mainly because, despite the considerable production capabilities, Romania is still a net importer of natural gas.

Within this context, we are expecting an increase of the price volatility with a downward pressure on producers and hesitation from the suppliers to hedge longer term position.

Based on the production estimations of each of the two main producers, who represent 95% of the gas produced in Romania, ANRE has set monthly quantities to be released on the centralized market for each product. These quantities are considerably higher than the average volumes historically traded on the centralized markets. In the last 12 months, an average of about 1.4TWh/month were concluded on the centralized markets, with more than 55% of the traded concluded in November and December 2020. Comparing the monthly gas release quantities for both producers, these are about 2.8TWh, 100% more than the above average monthly market volume. It is obvious that the liquidity of the Romanian wholesale market is expected to increase considerably starting the month of June 2020.

The effect is considerably greater for shorter, monthly, and quarterly products if we look at the volumes traded over the past 12 months on this type of products compared to the volumes that producers will release through this gas release program. However, the time set to launch this program is rather inappropriate for local producers, both the major and the smaller ones, because it comes after a mild winter in which consumption was not so high, the storage capacities are full, and these new quantities will put considerable pressure on the price, at least on the short term, creating the risk for some producers to reach their production cost limit.

In June, as an example, the first month of the gas release program, the maximum prices published by the producers for July delivery will be 95%*CEGH (July), which is now about 24.5 lei/MWh. Considering the volumes offered in June under this program, with storages full and typically low consumption during summer, we expect the forming price to be significantly influenced by these variables. This is more than 40% less than the average traded price for June.

To conclude, ANRE’s recent order could have significant medium- and long-term consequences. Foremost, the new provisions could indeed strengthen the Romanian gas market by increasing the trading levels and subsequently the market liquidity. Then, they will set out strong premises for building a market beneficial to the smaller producers and suppliers who could, within the new framework, better compete with the big players. Moreover, traders will be able to provide hedging tools based on market reference prices and respond in this way to the risk challenges various gas consumers may face.